HMO vs PPO vs HDHP: which plan type should your small business offer?

HMOs are lowest-cost but most restrictive (requires a primary care doctor and referrals). PPOs give more flexibility but cost more. HDHPs have the lowest premiums but highest deductibles — and they're the only plans that pair with an HSA. There's no universally 'best' option; the right choice depends on your workforce's health needs and your budget.

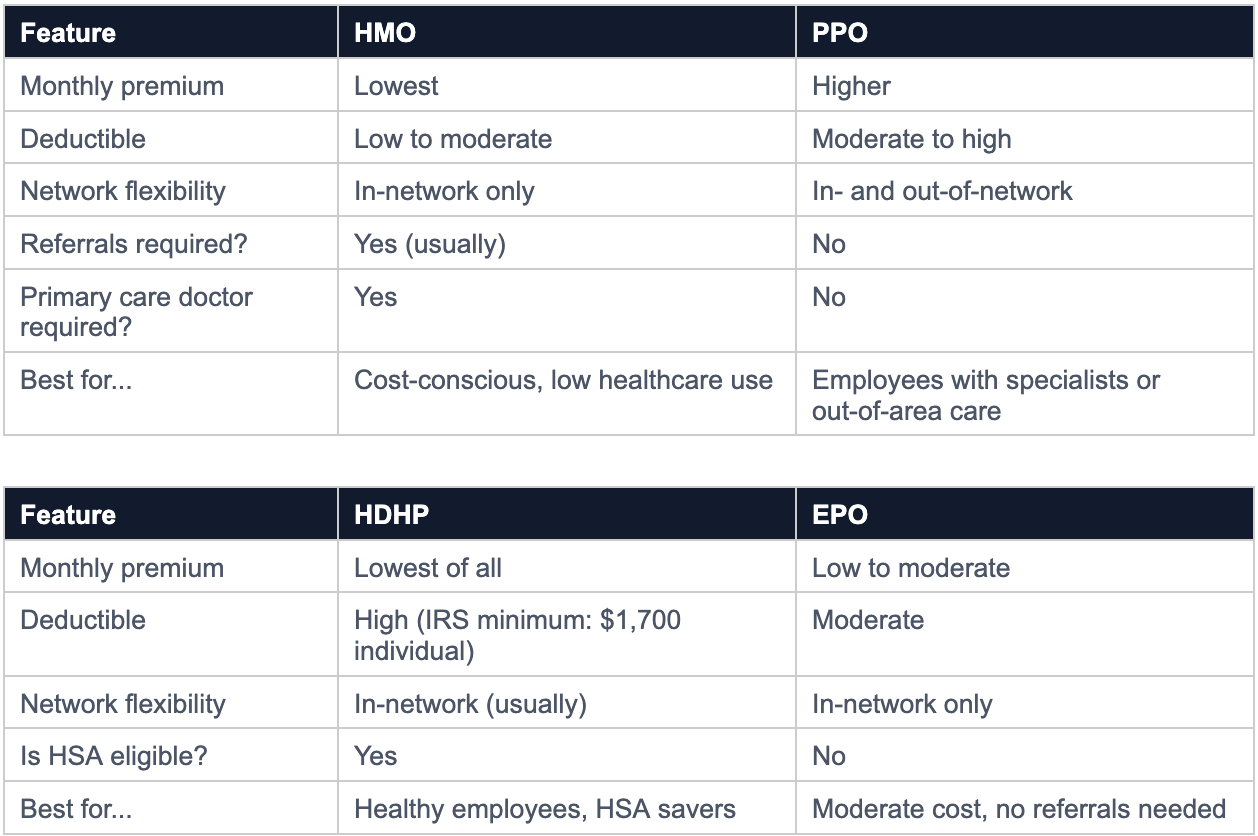

The three plan types at a glance

What brokers should know when presenting to SMB employers

Small business owners typically make benefits decisions based on three factors: premium cost, employee satisfaction, and administrative simplicity. Here's the framing that tends to land:

Lead with premium impact: For a 10-person company, the difference between an HMO and PPO can be $15,000–$30,000 per year in employer premium contributions. That number gets attention.

Pair the HDHP with HSA education: Employees often reject HDHPs because the high deductible sounds scary. Brokers who can clearly explain the HSA offset — and help employees understand the long-term savings value — see significantly higher HDHP adoption.

Know your workforce demographics: A team of 25-year-olds with minimal healthcare use is an ideal HDHP candidate. A workforce with older employees or families with kids may value the lower out-of-pocket exposure of an HMO or PPO.

Cost comparison scenario

For a 10-person company in a mid-cost market:

NOTE: New for 2026: HDHP eligibility just got broader

The One Big Beautiful Bill Act (OBBBA), enacted in mid-2025, made several meaningful changes to HDHP and HSA rules that take effect in 2026. Bronze-level and catastrophic plans available through the ACA Marketplace are now automatically treated as HDHPs, opening HSA eligibility to employees who previously couldn't contribute because their plan didn't technically meet the deductible threshold. Additionally, HDHPs can now permanently cover telehealth and other remote care services before the deductible is met — a provision that had been extended on a temporary basis for years and is now settled law. For brokers, this means a wider pool of employees can pair an HSA with their existing coverage, and the HDHP + HSA conversation is worth having with more clients than ever.

Frequently asked questions

Can a small business offer more than one plan type?

Yes. Many SMB employers offer a 'buy-up' option — a base HDHP with a PPO or HMO as an optional upgrade employees can choose by paying the difference in premium. This balances cost control with employee choice.

What's the minimum group size to offer group health insurance?

It varies by state, but most carriers require a minimum of 2 eligible employees. Some states allow groups of 1 (sole proprietors with employees).

Does the plan type affect dependent coverage?

Yes. HMO dependent coverage is limited to in-network providers. PPO plans allow dependents to see out-of-network specialists. This matters significantly for families with children who have specialists.