HSA vs FSA: which one is right for you?

The short answer

An HSA (Health Savings Account) rolls over year to year and is yours to keep forever. An FSA (Flexible Spending Account) is typically 'use it or lose it' by year-end. The biggest catch: you can only open an HSA if you're enrolled in a high-deductible health plan (HDHP).

The key difference in one sentence

An HSA is a savings account you own that grows over time. An FSA is an employer-sponsored benefit account you need to use up before the plan year ends.

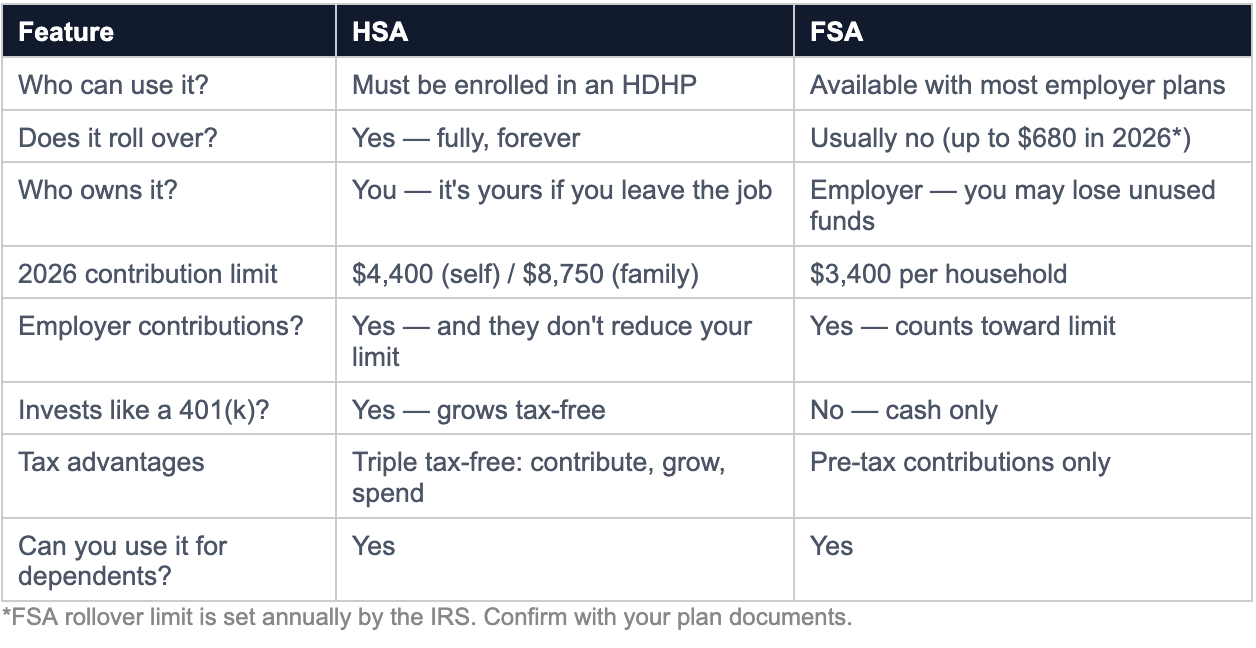

Side-by-side comparison

What can you spend HSA and FSA money on?

Both accounts cover a wide range of qualified medical expenses, including:

Doctor and specialist visit copays and coinsurance

Prescription medications

Dental and vision care (crowns, glasses, contacts)

Mental health services

Chiropractic care

Medical equipment (crutches, blood pressure monitors)

Over-the-counter medications (since 2020)

HSAs have one additional advantage: after age 65, you can withdraw funds for any purpose (not just medical) and pay only ordinary income tax — making it function like a traditional IRA.

Decision guide: which one is right for you?

Ask yourself these questions:

Are you enrolled in an HDHP? If no — you cannot open an HSA. An FSA is your only option.

Do you consistently spend your healthcare budget each year? If yes — an FSA's use-it-or-lose-it rule is less of a risk; take the immediate pre-tax benefit.

Are you building long-term savings or have low near-term healthcare costs? If yes — the HSA's investment and rollover features make it far more valuable over time.

Does your employer offer both? Some employers offer a Limited-Purpose FSA alongside an HSA — it covers only dental and vision, so you preserve HSA eligibility while still getting an FSA tax benefit.

Frequently asked questions

Can I have both an HSA and an FSA at the same time?

Not a standard general-purpose FSA. But if your employer offers a 'Limited-Purpose FSA' (dental/vision only) or a 'Post-Deductible FSA' (kicks in after you've met your deductible), you can hold those alongside an HSA without losing HSA eligibility.

What happens to my HSA if I switch to a non-HDHP plan?

Your existing HSA funds stay with you and you can continue using them for qualified expenses — but you can no longer make new contributions while enrolled in a non-HDHP plan.

What happens to my FSA if I leave my job?

Generally, you lose unused FSA funds when you leave. However, if you elect COBRA continuation coverage, you may be able to continue your FSA through COBRA.

What if I contribute too much to my HSA?

Excess contributions above the IRS limit are subject to a 6% excise tax. If you catch the error before filing your taxes, you can withdraw the excess and avoid the penalty.